November 24, 2022

I

Cathy He (OS Team); Bybit Research Team

Since DeFi summer brought about the 2020 bull market, everyone anticipated “institutional adoption” to come to DeFi. Integration between TradFi and DeFi mainly happened on the trading front, where centralized exchanges became a middle ground for TradFi crypto adoption. Market makers and proprietary funds alike began executing carry and price arbitrage on centralized and decentralized venues. To accommodate billions of dollars of flow, key on-chain trading infrastructure projects were incubated and funded by these institutions. An example of such an infrastructure is Pyth, where 70+ institutional trading firms, with the likes of Jump Crypto and DRW Cumberland, publish price discovery and create market efficiency across different venues. The completion of decentralized infrastructure in financial trading allowed sophisticated trader flows to enter crypto native markets.

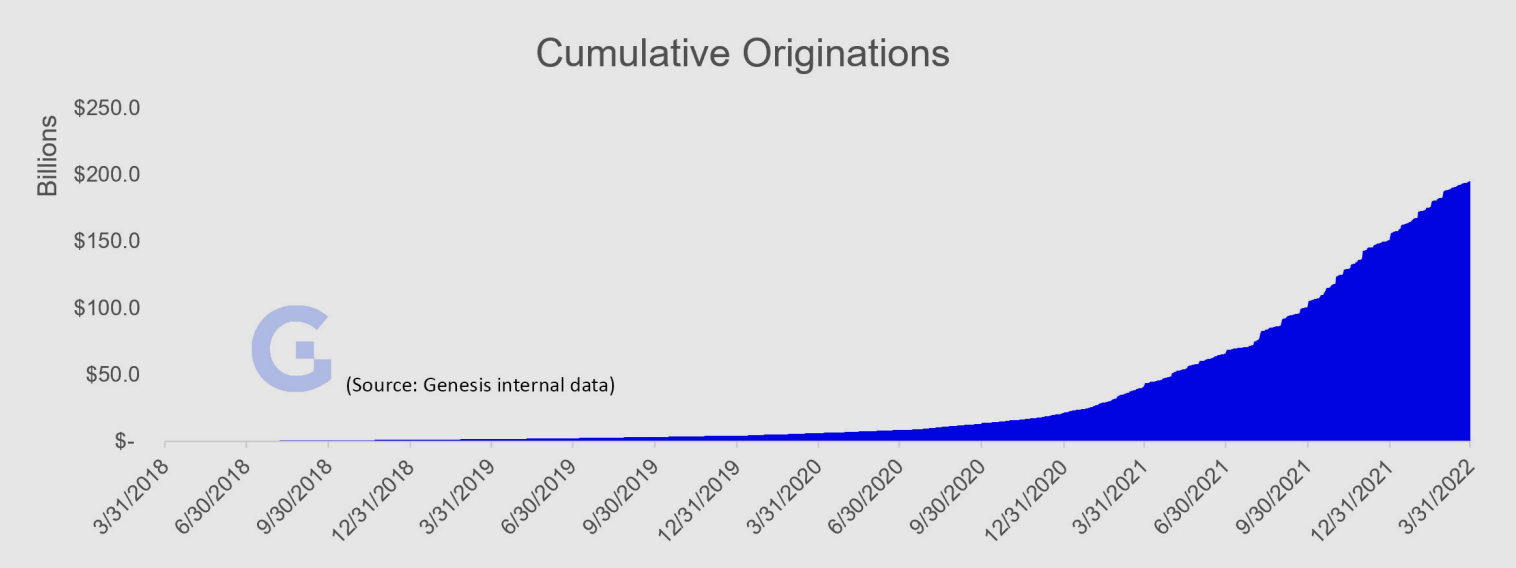

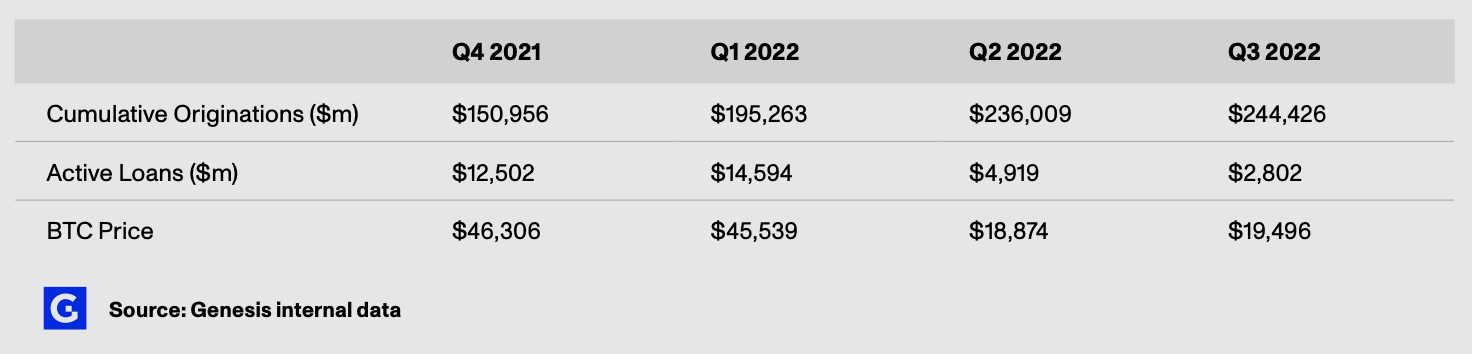

Looking past financial trading, there is a second type of institutional capital brewing in DeFi — these are private credit funds that received traction after the centralized lenders imploded in May 2022. Before the liquidity crunch in May this year, centralized lending desks originated a phenomenal amount of crypto loans, for example, Celsius, Genesis, and BlockFi together issued $45.6 Billion of loans in Q1 2022. Main customers for these loans were institutional traders, who were willing to pay 10%+ APY on daily liquidity.

Source: Genesis Investor Data

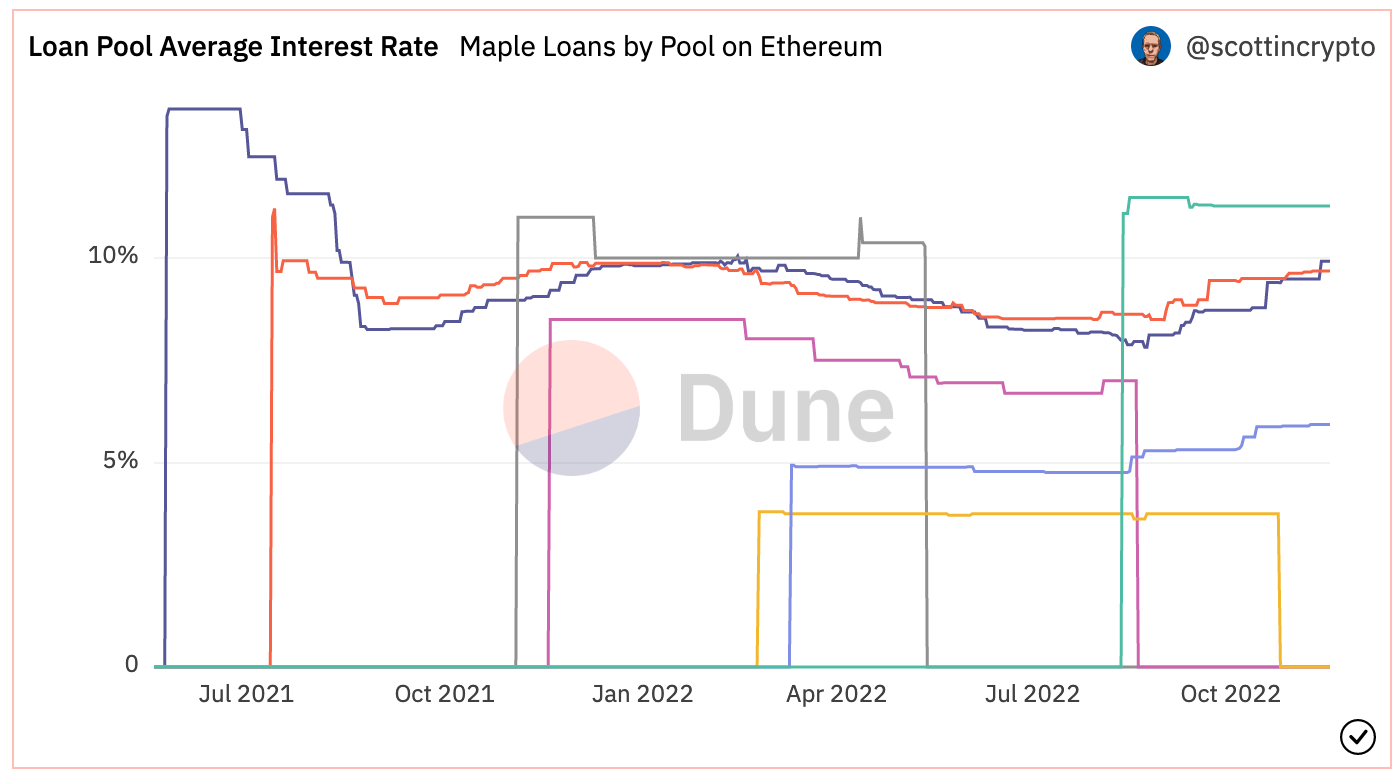

With the fast de-leveraging of these centralized entities, there was a void of liquidity in the market and profitable crypto-native institutions turned to DeFi solutions to fill in the space. The market saw the rise of Orthogonal Credit, M11 Credit, and Blocktower Credit, which are credit funds that provide direct lending on venues such as Maple finance to market makers, e.g. Wintermute, Auros and Flow Traders, allowing them to draw USDC at 8.5-10% and draw wETH at 5-6%.

Source: @scottincrypto, https://dune.com/scottincrypto/Maple-Deposits

Asset management products have also moved on-chain, democratizing investment strategies that historically were only available to large institutional clients. Leveraging smart contracts and unique crypto-native non-linear yields, strategies such as DeFi Option Vaults (DOVs) saw breakout volumes in 2021, with $1 Billion in Total Value Locked (TVL) at its peak. Vaults like Ribbon Finance, Friktion, and Antimatter, provide simple UI/UX to allow retail investors to tap into vanilla option premiums. From underwriting out of money covered calls and vanilla puts, retail investors saw these option premiums reeling in 20 to 40% of returns at the time, which looked very competitive and more sustainable compared to incentive based yield farms. On the back of these retail underwriting, institutional options market makers would buy the entire vault of options and sell on exchanges such as Deribit which saw 90% of total crypto option flow at some point. Currently option vaults face lower volumes due to several reason:

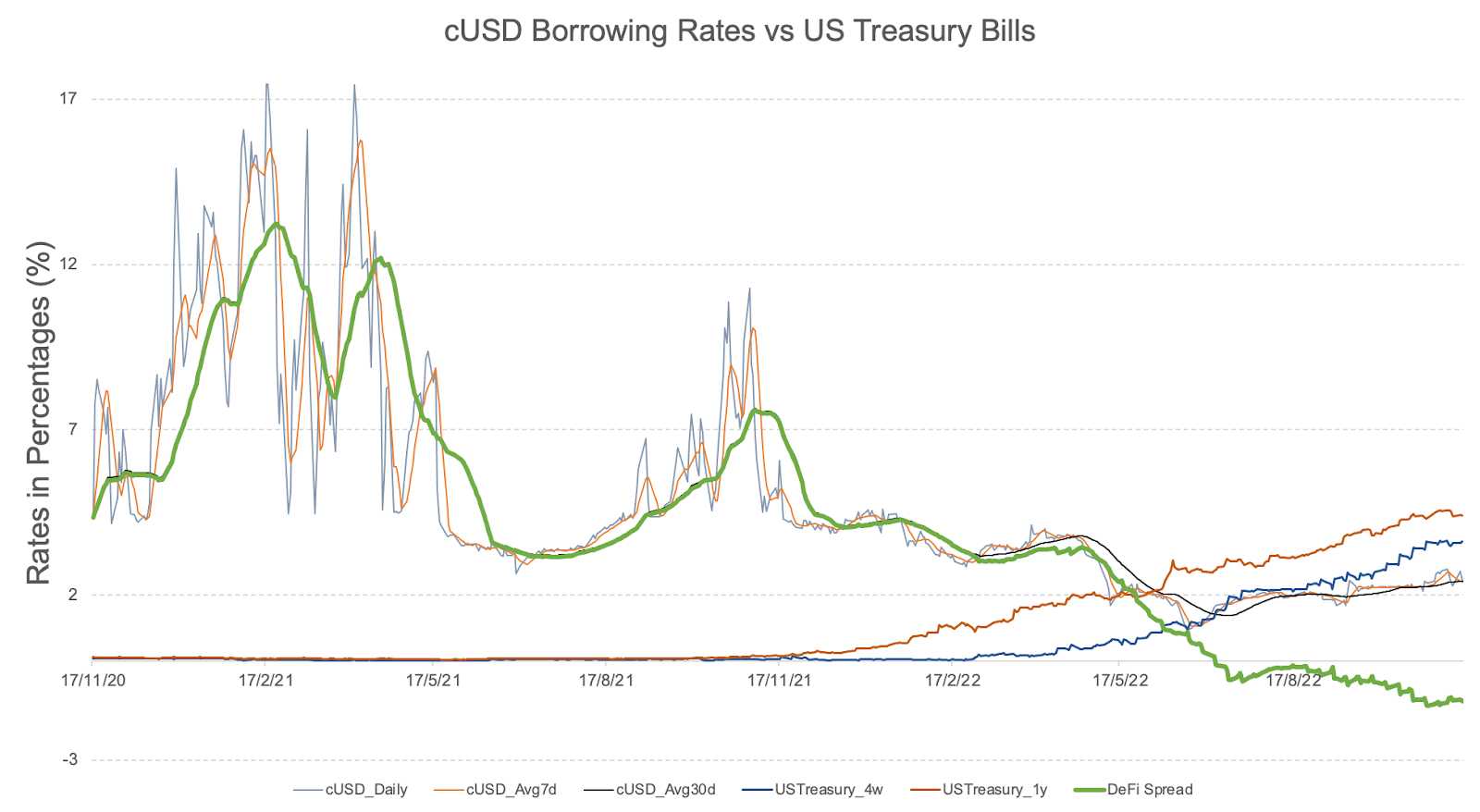

While DeFi volumes today depend on trading players whose health dictates how active DeFi is, a more balanced ecosystem would welcome players beyond traders, who can leverage the efficiency and transparency of this new paradigm. With the US Fed Funds target rate turning to 3.75 to 4.00%, the DeFi spread (the difference between DeFi borrowing rate and US treasury) has turned to -1.2%, which begs the question — Does it still make sense to invest DeFi capital in Compound’s cUSDC pools where yields are less than 2%? Where will DeFi capital go?

Source: St Louis Fed - https://fred.stlouisfed.org/series/DTB4WK, @tt_taylor https://dune.com/queries/30619/61723

With the above background and questions, this report will delve into the current development of DeFi’s real-world usage, difficulties that hinder such developments, and possibilities in DeFi’s integration with TradFi.

The first phase of DeFi arguably revolved around TradFi capital flows into DeFi, as well as how new capital is deployed to bring TradFi functions to DeFi, including exchanges, trading, lending, derivatives, payments, etc. So far, DeFi applications have been mainly used by crypto-native users. Unfortunately, due to an extended bear market, DeFi usage declined in the face of muted speculative activities. As a result, DeFi protocols turned their focus from retail investors to institutional investors and from crypto trading to tokenized real assets.

The next phase of DeFi seems to be for native DeFi protocols to add the support of real-world assets and enlist real-world players as DeFi users. In this section, we will dive deeper into how DeFi currently interacts with real-world assets.

In order to expand its usage outside the crypto-native community, DeFi ventured into the traditional world of finance. DeFi’s real-world lending caters to institutional needs, for simplicity DeFi’s real-world lending in this article only refers to DeFi protocols’ lending to real-world institutions, excluding lending to retail investors.

Top DeFi lending protocols, such as Aave and Compound, offer on-chain over-collateralized loans without the procedures of KYC and credit assessment. In contrast, real-world institutions that are sensitive to capital efficiency loathe over-collateralized loans due to lower leverage, leading to the emergence of DeFi protocols that lend solely to real-world players with under-collateralized or un-collateralized loans, such as Maple Finance.

Despite low capital efficiency, over-collateralized loans in DeFi have a role to play in real-world lending due to lower borrowing rates, with MakerDAO being the pioneer and leader. However, over-collateralized loans often only attract large financial institutions, such as banks, with premium assets as collaterals but not smaller-sized private credit firms. For example, without credit assessment, MakerDAO only charges 30 bps above 5-year treasury loans for its lending to syndicated loans managed by Huntingdon Valley Bank, which is low compared to around 140bps credit risk premium for high-quality bonds.

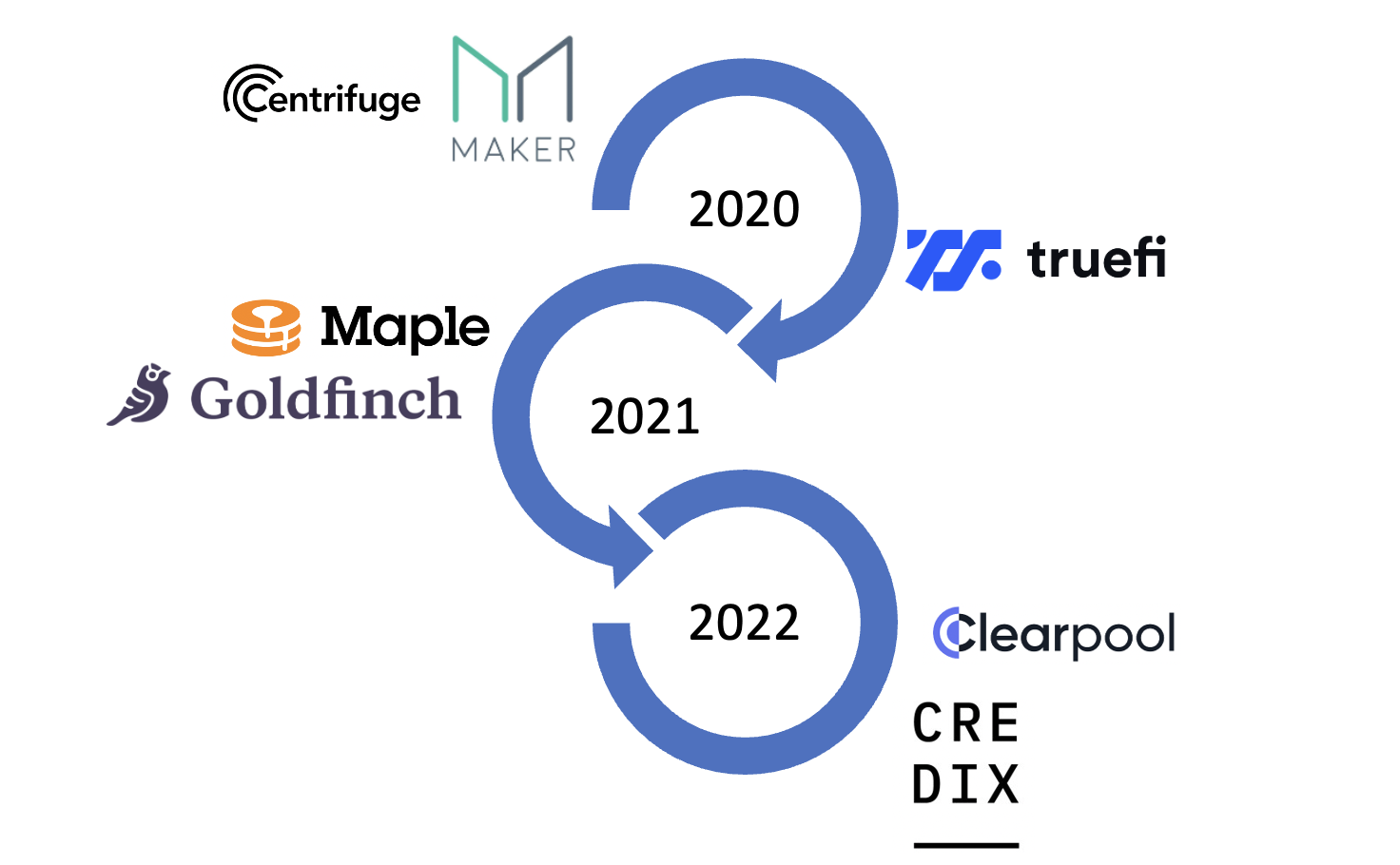

With the assistance of real-world asset pools on Centrifuge, MakerDAO ushered in real-world lending back in 2020 on the back of the approval of the proposal for the DAO to onboard off-chain real-world assets (RWA). On the other hand, uncollateralized institutional lending came to light with the launch of TrueFi in Nov 2020 and Maple Finance and Goldfinch in mid-2021. Stepping into 2022, as DeFi space reels from crypto winter, Clearpool, and Ribbon Lend, among other protocols that target institutional borrowing, continue to enter the space.

Source: https://makerburn.com/#/rundown (data as of Nov 16, 2022)

The most prominent protocol with over-collateralized real-world lending is MakerDAO. As of the time of writing, MakerDAO owns eight RWA pools with an outstanding supply of DAI to the tune of$336.7 million. Among them, four lending pools are based on RWA pools from Centrifuge, with collateral including loans to real estate investors, freight invoices, short-term trade receivables, and revenue-based financing assets. Another three lending pools are through a trust structure, with cooperation from 6s Capital, a fund that lends to real estate developers, Huntingdon Valley Bank (HVB), a bank located in the United States, and lastly, Societe Generale, a prominent French bank. The last RWA pool is made up of investments in a high-quality bond scheme with Monetalis to seek higher yields in TradFi.

Centrifuge plays a critical role in MakerDAO’s RWA ambition by tokenizing collateral assets. Investors are separated into two tranches, junior and senior tranches. The junior tranche is open to professional investors looking for higher returns but comes with higher default risks. The RWA pools on Centrifuge cover industries such as real estate bridge loans and fintech debt financing, among others.

While most end borrowers may be linked with real-world usage, the largest RWA pools are Monetalis and the HVB pool, representing 89.3% of the total RWA pools’ DAI supply as of the time of writing, suggesting that Centrifuge-connected pools are a minority among RWA pools.

Moreover, large RWA pools on MakerDAO in connection with Centrifuge were launched in 2020 or early 2021. As uncollateralized lending protocols gained traction in late 2021, MakerDAO lost its luster due to lower leverage from over-collateralized loans, while small borrowers flocked to under-collateralized lending platforms.

It is important to note that the supply of DAI on RWA accounts for a small fraction of the total DAI supply, approximately 5.4% as of the time of writing. However, with continuous investments in treasury yields, the RWA proportion is likely to rise in the foreseeable future.

All in all, despite early-stage developments, MakerDAO’s RWA scheme has set a great example for the integration of TradFi and DeFi. Not only do real-world players borrow on the platform, but MakerDAO, sitting with more than 3 billion PSM reserves in USDC, has started to seek yields from traditional assets. As we mentioned at the beginning of this article, TradFi capital used to flow into DeFi for higher yields. With treasury interest rates hiking and DeFi yields shrinking, it is natural that DeFi capital flows back to TradFi, ushering in a new era of TradFi-DeFi integration.

Source: rwa.xyz (data as of Nov 16, 2022)

Real-world assets collateralized by DeFi institutional lendings are mainly private credits. As of the time of writing, there are active loans amounting to $359 million with an average APY of 11.47% that offer on-chain loans to real-world borrowers. The top real-world borrowers are from fields such as fintech, real estate, and carbon projects, among others.

Under Collateralised Lending Protocols

TVL (USD)

Loan Value Outstanding (USD)

Lenders

Maple Finance

296.3m

279m

Private credit firms, Crypto market makers

TrueFi

38.94m

15.14m

Market makers, private credit firms

Clearpool

23.8m

7.5m

Market makers

Goldfinch

20m

5.2m

Private credit, asset-based loans

Ribbon Lend

28.5

28.5m

Market makers

Source: Dune Analytics@blakewest; Protocol Websites (data as of Nov 14, 2022)

Maple Finance is the leader that offers under-collateralized lending from DeFi to real-world borrowers, with the highest TVL at around $136.2 million. Uncollateralized lending on DeFi targets institutional investors, both crypto-native and real-world players. After rigorous KYC and credit assessment, institutional investors can create a pool on Maple Finance, TrueFi, and ClearPool for borrowing from DeFi users.

However, these under-collateralized lending platforms may not directly serve real-world borrowers. Crypto market makers form a large portion of borrowing demand on TrueFi and ClearPool, which strictly do not qualify as real-world borrowers. On the other hand, Goldfinch, which promotes itself as a true lender to developing countries for real yields, integrates better with real-world players and may continue to drive value to the platforms.

Credix is a new institutional lending protocol launched this year on Solana, with a similar model to Goldfinch, connecting global capital to Latin American Fintech borrowers. Credix sets itself apart from the previously mentioned institutional lending protocol by underwriting over-collateralized loans themselves, lowering the default risks for liquidity pool investors while offering an attractive yield.

Moving the trading of real-world assets on-chain is another way to expand DeFi’s real-world usage. The possible real-world assets include equities, currencies (FX), commodities, and complex derivatives, among others. Synthetix, a popular synthetic trading DeFi platform, offers derivative tokens, dubbed synths, to trade crypto and FX, mainly USD, EUR, and INR, while Gains Network includes trading pairs of crypto, FX, and equities. Tokenizing real-world assets lays the foundation for real-world users to trade traditional assets with no intermediaries.

At this juncture, tokenized equities might not attract users due to a series of issues, such as dividend distribution and asset custody. However, DeFi might play a role in facilitating cheaper trading of FX pairs for real-world users, as traditional banks charge high spread costs for retail users. Furthermore, FX volatilities amidst the U.S. monetary tightening cycle leave currencies from developed and emerging countries volatile. FX trading on DeFi enables users to hedge or trade their home currencies with minimal spreads to prevent wealth reduction from currency depreciation. As a highlight, USD/JPY and GBP/USD registered over 232 million and $103 million trading volume in the past 30 days on gTrade, representing around 12.6% and 5.6%, respectively, suggesting a blooming FX trading on DeFi platforms.

While we have seen the adoption of trading and lending DeFi protocols with real-world players, DeFi's integration with TradFi is still in the early stages. DeFi categories other than trading and lending have not seen the same level of integration with TradFi. As such, we will look into what disconnects DeFi from TradFi in the following section.

Drawing parallels to traditional financial services, institutional services can fall into the following four categories: trading, lending, investment products, and transaction banking. So far, trading and lending have found the most product market fit in decentralized finance; the appetite for integration seems to be slower in other corners of financial services, and it is worth looking into the roadblocks preventing further integration.

Crypto regulation today remains at rudimentary levels, where most countries’ governing bodies only have concrete guidelines around Anti Money Laundering (AML) practices. As of today, this rudimentary level of regulation has allowed big banks such as JPMorgan to use public blockchain e.g. Polygon as a settlement layer to enhance transparency and efficiency. These trials using a sandboxed environment, albeit exciting steps towards more DeFi adoption, are more of a feature (fractional reserve) in commercial transaction banking than integration of the capital markets. Lack of regulation is preventing TradFi players from using decentralized venues for sourcing and deploying capital.

Few countries have more sophisticated regulations regarding crypto investments, for example:

One current solution to the regulatory barriers is Securitize, a KYC layer that allows off-chain real-world assets to accept DeFi capital from compliant investors. The platform has been in the headlines for tokenizing KKR’s healthcare fund, which is one of the first examples of adoption from large private equity players. The platform not only checks whether the investor complies with AML and OFAC requirements, but it also checks whether an investor is fit to participate in the offered investment-grade products. In the US, an accredited investor must have $1 million of net worth, at least $200,000 of income for the past two years, or financial practitioner licenses such as Series 7, 82, 65. This approach is a hybrid approach to DeFi and may be seen as a compromise that might have trouble convincing both traditional institutions and DeFi native players to adopt it. Crypto native KYC solutions using zero-knowledge, such as zkPass, could be the beginning of the end-game for the regulatory dilemma.

Often seen as the double-edged sword of DeFi, vulnerable smart contracts have continuously been targeted by malicious hackers and pose the largest inherent risk in the industry. 2022 saw a total of $3 billion stolen from different attacks, where October alone took $718 million from the system across 11 hacks. Reportedly, white hat hackers have been working through a record-high backlog of hack analysis and mitigation. Common vulnerabilities include:

While web3 development has attracted 10x interest since 2018, most of the investment in security has focused on ensuring protocols and their later updates are audited and trusted by their users. With the explosion of new protocols in DeFi, top auditing firms are known to have congested sales pipelines. However, once smart contracts are deployed, there is a lack of investment for on-chain activity monitoring and post-attack retrieval of funds. An example is when DFX – an FX DeFi protocol – was recently hacked, the team was only able to react 20 to 30 minutes after the hack had been detected. The scale of re-investment into security is very different from TradFi and CeFi players, who take an active engagement model spending billions on cyber security budgets.

For active mitigation near real-time, smaller crypto native players like Hackless (a previous EthLisbon hackathon winner) have been monitoring mempools to detect unusual on-chain behaviors, sandwiching malicious transactions, and migrating funds to a safe haven. For post-breach remediation, investigative firms such as Chainalysis (invested by GIC, Blackstone, BNY Mellon) and TRM Labs (invested by Goldman Sachs, Citi, Amex, and Paypal) both launched an incident response division this year to serve institutional clients. The effort tries to to recover the funds by tracking down transaction trails, e.g., Nomad bridge hack and Slope Wallet compromise. Scalable pre-deployment auditing, real-time attack mitigation, and post-breach investigation are the three key areas of development essential for integration with large TradFi institutions.

DeFi yields come from validator rewards, lending, and trading rewards such as LP tokens, as well as more “degen” liquidity incentivisation rewards (many of those are battling downward token price pressure in the long term). Through this year’s two large liquidity crunches - some yields have stayed resilient, especially in validator rewards where liquid staking yields for ETH have returned to 10%. Such resilience in crypto native network yields can provide more comfort for institutional capital to enter the space. However, there is still not enough yield-generating assets on-chain for institutional appetite, and the negative DeFi spread presents an unique timing to examine what are the challenges to bring real-world assets on-chain.

The biggest bottlenecks to bringing more real world assets on-chain are asset origination and real-time data oracles. Firstly, real world asset yield opportunities have not seen a lack of US dollar liquidity since quantitative easing began in March 2009, and hence there was little incentive to cross both regulatory and security hurdles to be on the blockchain. Simply put, capital was cheap, it did not make sense for good quality real world assets to seek on-chain funding even in stablecoins. This phenomenon has only started to change recently, when the Fed started reversing the size of its balance sheet this year. While on-chain liquidity is seeing tightening post-FTX blowup, real-world assets will continue to increase their interest in crypto funding if negative DeFi spread persists.

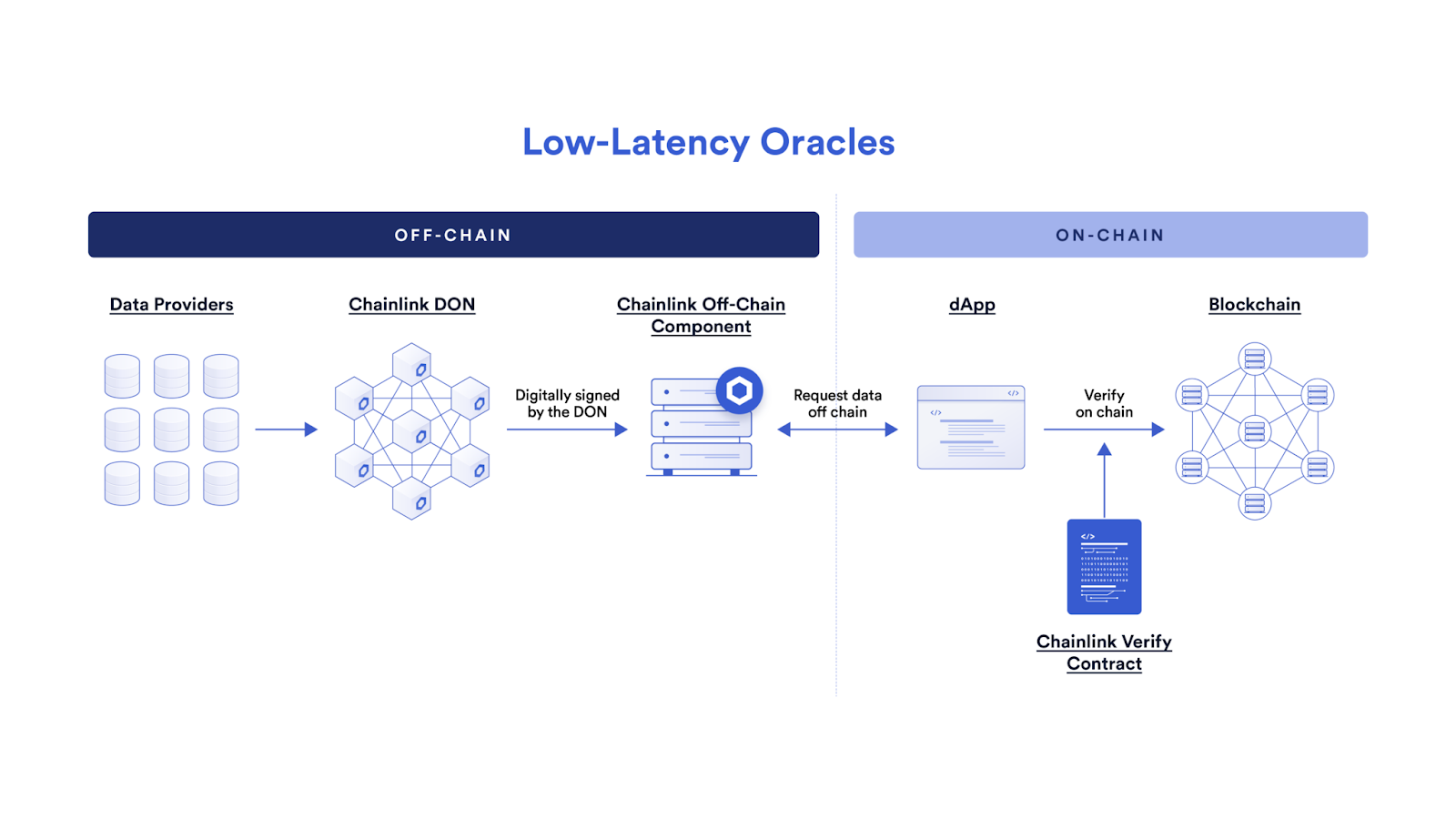

Secondly, origination for more diverse assets is highly dependent on access to and integration with good quality real world assets. These deals require more integrated oracle infrastructure to improve off-chain data feeds with on-chain execution, which require consensus from stakeholders on what data is required in each of the DeFi applications. Some ideas are data for the underlying real world asset, the inner workings of the deal terms that may include deterministic payouts, as well as state feeds for collateral and credit assessments e.g. proof of reserve. Interestingly, proof of reserve recently became more widely adopted as industry standard as centralized exchanges such as Bybit are collectively restoring trust in the crypto industry.

Source: Chainlink, https://blog.chain.link/low-latency-oracle-solution/

Despite the current state of DeFi’s real-world functionalities on a global and macro scale, we believe there is more room for integration between the two spaces.

As DeFi yields have ground lower, global yields have been rising against the restrictive monetary policy from major central banks. As a result, seeking yields from government or corporate bonds for DeFi protocols might be a rational maneuver. As government bonds remain largely inaccessible to most retail investors, tokenizing risk-free investments such as government bonds may attract users to invest cash in the blockchain.

In addition, when: (1) higher yields from under-collateralized lending that pay for credit risks and (2) yields from liquidity provision that factor in impairment loss are excluded, the real yield from USDC lending offered by lending protocols such as Aave is only at 0.31% as of the time of writing. In comparison, 3-month and 6-month U.S. government treasury yields are at 4.16% and 4.53%, respectively, remarkably surpassing the yields on Aave.

As such, DeFi protocols that purchase U.S. treasury bonds in secondary markets for asset tokenization might attract users to their platforms with higher yields. That being said, there are legal and regulatory challenges ahead, but the trend of asset tokenization in DeFis continues to grow.

Uncollateralized institutional lending offers a significantly higher rate than collateralized protocols such as Aave. Goldfinch, for example, offers yield for its senior tranche at over 13% APY, project by project, with 8% interest payments in USDC and 5% in GFI, its native token. The higher yield may attract capital amidst plunging DeFi yields.

Despite plunging TVL and outstanding debt, Credix, an institutional lending protocol newly launched in June, continues to close new partnerships, such as the upcoming $150 million pool launch with Clave, an Argentinian fintech company, indicating demand for real-world lending from Latin America. What’s more, Maple Finance’s new pool that targets embattled Bitcoin miners has received overwhelming applications, further speaking of massive potential from institutional lending. The popularity of Maple Finance for miners reinforces that traditional corporate finance has leaned toward quality and large-scale firms while embattled small firms are not taken care of. As such, the institutional lending market has great potential by serving real-world players, which might attract new protocols to innovate in this space.

That said, the design of under-collateralized institutional lending has its drawbacks, including off-chain diligence and low default protection. As a highlight, native tokens staked dropped in value upon borrowers’ defaults, leading to low coverage from defaulted loans.

Over-collateralized lending may serve real-world players due to its low yield, as mentioned earlier. High yields from uncollateralized lending target small to medium firms, while collateralized lending with lower borrowing rate serves financial institutions or investment managers which hold premium assets. At this juncture, more DeFi protocols aspire to issue their stablecoin, including GHO from Aave and Curve’s impending stablecoin. GHO’s business model is closer to the one of MakerDAO and might launch RWA modules as Aave’s business model continues to evolve. Moving forward, more financial institutions like JP Morgan will try out blockchain technology. The CDP protocols, such as MakerDAO, as one of the most established DeFi categories, in our view, may attract them to experiment first.

Source: IMF

Traditional financial institutions can reduce operational costs by leveraging DeFi technology. Based on the IMF's report, compared to traditional financial institutions, DeFi has significantly lower labor costs, with smart contracts governing on-chain transactions and validators performing verification and record retention. Traditional finance, which is profit-driven, can simply leverage blockchain technology to save labor costs and further boost its profits. As such, DeFi protocols that help onboard traditional financial institutions to blockchains will thrive. An example is Quant Network, which gains traction by connecting traditional financial institutions with multiple distributed ledger networks.

As insolvency events continue to steal the limelight, DeFi has taken a hit from plunging TVL and user exodus. However, the long-term secular trend that DeFi will drive value from real-world integration is unstoppable. We have shared our thoughts on how and why further integration between TradFi and DeFi can and should occur, and more possibilities await for industry players to explore. In our view, the next DeFi Summer will come from deepening integration between DeFi and TradFi.